Servicios Personalizados

Revista

Articulo

Español (pdf)

Español (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Enviar articulo por email

Enviar articulo por emailIndicadores

-

Citado por SciELO

Citado por SciELO

Links relacionados

-

Similares en

SciELO

Similares en

SciELO

Compartir

Permalink

PermalinkVisión de futuro

versión impresa ISSN 1668-8708

Vis. futuro vol.11 no.1 Miguel Lanus ene./jun. 2009

ARTÍCULOS ORIGINALES

Costos en el Sector Público Importancia de la Relación con la Presupuestación

Tiberio Julio César

Universidad de Buenos Aires- Facultad de Ciencias Económicas- Av. Corrientes 6041 2do. Piso Dto. B- C.P: 1414 - Ciudad Autónoma de Buenos Aires- Teléfono: (011) 4855 - 5023

E-mail: jctiberio@uolsinectis.com.ar

RESUMEN

El trabajo tiene el propósito de divulgar la importancia del tratamiento de los costos en el sector público, haciendo conocer la necesidad de analizar en profundidad y reflexionar sobre la importancia de su correcta utilización a fin de satisfacer la mayor cantidad de bienes y servicios que el Estado (Nación - Provincias - Municipios) a través de sus programas de gobierno incluidos anualmente en el presupuesto público permitan concretar las demandas que la población tiene derecho a recibir, dado que la misma aporta los recursos necesarios para tal fin.

Para ello se seleccionaron trabajos de distinguidos profesionales que han advertido la importancia que el tema merece.

Asimismo se incorporaron métodos o sistemas de costos que permitirán concretar una propuesta presupuestaria cuya prioridad está asentada en la eficacia, la eficiencia y la economicidad en la obtención de los recursos públicos y el destino de los gastos que permitan el cumplimiento de las metas previstas para el cumplimiento de las finalidades que persiguen como objetivo indelegable lograr el bienestar de la población.

Considerando que los planes estudios universitarios de las Carreras de Ciencias Económicas no muchas veces ponen énfasis en la importancia del Sector Público, muy especialmente en la de Contador Público, se estima necesario que los estudiantes y los jóvenes profesionales adviertan la importancia que tiene el manejo de la cosa pública y la estricta relación que existe entre tributación - evasión - gastos y costos necesarios para satisfacer las necesidades de la comunidad, motivo de nuestra preocupación.

PALABRAS CLAVE: Presupuesto; Costo; Gasto; Bienestar; Comunidad

INTRODUCCION

En oportunidad de elaborar el libro Casos Prácticos de Contabilidad Pública que publicamos con el Profesor Horacio Francisco Mastrantonio en 1990 con el apoyo de Ediciones Macchi, nos ocupamos del tema de los costos en la programación del Presupuesto Público.

En el mismo al expresar un concepto de Presupuesto por Programasseñalamos: es la expresión de las asignaciones presupuestarias, practicadas en función de los planes de gobierno, para un período determinado en los distintos ámbitos de su competencia, de modo de lograr el máximo cumplimiento de los mismos al mínimo costo.

Se tuvo en cuenta muy especialmente en esos momentos la importancia que las Normas para la Confección del Presupuesto fijadas por la Secretaria de Hacienda de la Nación daba a dos temas específicos para la aplicación del esquema de Presupuesto por Programas: costos y control de gestión.

En este trabajo nos referiremos al primero de los nombrados, al efecto señalábamos:

Como parte integrante de la presupuestación por programas, es necesario contar con un sistema que permita medir el costo de los diferentes niveles de programación.

La utilización de dicho sistema posibilitará establecer el grado de eficiencia en el cumplimiento del programa, y deberá adaptarse a las diferentes modalidades de detalle de acuerdo con las características, importancia y fines de cada organismo.

El sistema presupuestario permite aproximarse a los costos a través de los gastos previstos o efectuados, agrupados mediante la clasificación económica y por objeto del gastos.

El costo total de un programa o actividad estará dado por los gastos previstos o efectuados en su ejecución, ajustado en función de las diferencias (costos sociales o de oportunidad, consumo o utilización de los bienes, amortización, etc) y, de los costos indirectos originados en los gastos de aquellos programas, fundamentalmente de conducción y administración, cuya acción es de apoyo a otro conjunto de programas, entre los que deben distribuirse.

El costo unitario surgirá de la relación de la meta del programa o resultado de la actividad cuantificados a través de alguna unidad de medida, y el costo necesario para lograrlas.

En la misma publicación cuando se incluyeron los lineamientos generales acerca de la elaboración del Presupuesto por Programas y muy especialmente las ventajas de su aplicación que Gonzalo Matner en su libro Planificación y Presupuesto por Programas de Editorial Siglo XXI - México 1971 describe con gran precisión, señalando con respecto al tema de este trabajo: Oportunidad de reducir costos.

Siguiendo el análisis de otros tratadistas podemos señalar, que desde un punto de vista general, costo es sinónimo de esfuerzo.

Esta definición es suficientemente amplia para involucrar tanto al esfuerzo físico, moral e intelectual como al económico.

Pero mientras los primeros no son mensurables en unidades de valor, aunque sus consecuencias puedan serlo, el esfuerzo económico se representa siempre de esa forma.

Económicamente, pues, costo es sinónimo de gasto, esto es, de sacrificio. Pero ese sacrificio debe haberse producido en pos de un objetivo determinado, lo cual diferencia originariamente el costo de la pérdida simple o pura, que depende de factores eventuales o ajenos a la persecución del objetivo.

De lo antedicho surge que, económicamente hablando, costo es el sacrificio de riqueza que se incurre en pos de un objetivo determinado.

Como los objetivos varían según las características de los entes que los persiguen, trataremos de clasificar los entes en función de dichos objetivos, a fin de interpretar primariamente la índole de las erogaciones en que incurren, es decir, sus costos.

Los entes (y su representación patrimonial, las haciendas) de erogación tienen como principal objetivo la satisfacción de sus necesidades.

Las hay privados y públicos, pudiendo los primeros ser a su vez individuales o colectivos.

El típico ente de erogación privado individual es el ser humano individualmente considerado. Su objetivo es la satisfacción de sus necesidades y la actividad que desarrolla tiende a obtenerla.

Las erogaciones en que incurre para ello, es decir, su costo, toman la forma comúnmente denominada costo de vida.

Se trata de erogaciones simples que representan, en casi todos los casos, mermas en el patrimonio del ente directamente cuando se incurren.

Del mismo modo ocurre con los entes de erogación privados colectivos. Como puede ser una asociación civil de carácter mutual.

Su objetivo es la satisfacción de las necesidades de sus asociados y las erogaciones en que incurre constituyen el costo del servicio mutual que prestan.

Su objetivo es la satisfacción de las necesidades de la comunidad a la que representan y las erogaciones que realizan en tal sentido constituyen el costo de la administración de la cosa pública y de la prestación de los servicios comunitarios.

Las actividades que los Estados desarrollan para cumplir estos objetivos pueden ser más o menos complejas y ello incidirá, por supuesto, en la conformación de las erogaciones en que incurran.

La característica distintiva de los tres tipos de entes que hemos mencionado es la ausencia del fin de lucro.

Cuando éste aparece, es decir, cuando el objetivo del ente es el aumento de riqueza, estamos en presencia de los entes (y sus haciendas) de producción.

El concepto de producción coincide aquí con el de aumento de riqueza.

Teniendo en cuenta lo antedicho, el costo económico no es sólo sacrificio de riqueza presente, sino también de expectativas concretas de riqueza futura.

Costo económico es, pues sinónimo de sacrificio económico

En nuestro ámbito de acción, las Ciencias Económicas, no debe perderse nunca de vista el objetivo económico de la actividad que se desarrolla.

De este modo el estudio del costo por sí mismo no constituye sino una versión teórica, carente de utilidad.

Su determinación y control deben hacerse en función del mejor cumplimiento del objetivo del ente que lo incurre.

Así, en los entes de erogación, se hará en función de la satisfacción más racional de las necesidades; y en los de producción, en función de la obtención más racional del lucro.

Si quisiéramos condensar en una sola definición todos los conceptos analizados, podríamos decir, sin pretender que sea la mejor que:

Costo es el sacrificio económico originado en el desarrollo de determinada actividad, a través de la cual se busca cumplir con el objetivo dado.

Por último cabe decir cundo se habla de costo en general, no se particulariza con respecto al cumplimiento total o parcial del objetivo o al desarrollo total o parcial de la actividad.

Pero va de suyo que ambas referencias están implícitas en la definición que hemos dado, de manera que ella incluye tanto el concepto de costo total, global, esto es, referido al universo de actividad o a la plenitud del objetivo, como el de costo unitario, es decir, referido a cada un de las unidades en que puede dividirse tal universo.

Factores generadores del costo. Su componente físico y monetario.

En la formación del costo los factores básicos de la Economía son tres:

-

Naturaleza; 2) Trabajo; 3) Capital

Los factores generadores del costo son en realidad seis:

Tres primarios: 1) Naturaleza; 2) Trabajo; 3) Capital

Tres derivados: 1) Materiales; 2) Equipos; 3) Servicios

Constituyen los grandes factores de todo costo presente.

Cada uno de esos factores se halla formado por dos partes o componentes: uno físico, representado por la cantidad de unidades del factor utilizadas; y otro de valor, que al expresarse usualmente en términos de moneda suele denominarse monetario, representativo del precio de cada unidad del factor.

Aquí tenemos la base del actual sistema de Presupuesto por Programas:

-

La programación, presupuestación (previsión del grado de cumplimiento), ejecución, evaluación y control físico: cumplimiento de metas. Expresados en unidades.

-

La programación, presupuestación (asignación de créditos) ejecución, evaluación y control financiero: resultado presupuestario: (económicos y financieros). Expresados en moneda.

Por todo lo expresado en los párrafos anteriores nos permite señalar la importancia de la aplicación de las 3E en las normas previstas en la Ley Nº 24.156 de Administración Financiera y de los Sistemas de Control del Sector Público, cuyo artículo 4º señala que la misma debe garantizar los principios de:

-

Legalidad

-

Regularidad Financiera

-

Eficiencia

-

Eficacia y

-

Economicidad

A efectos de una mejor ilustración dejamos bien claro los conceptos de los tres últimos que están concretamente referidos al tema motivo de este trabajo.

Con respecto a su directa vinculación con la Cuenta de Inversión prevista en el Artículo 75º inciso 8) de la Constitución Nacional, y los comentarios que debe incluir la misma en función al Artículo 95º de la Ley Nº 24.156 (LAFySCSPN), ésta última expresamente solicita:

b) el comportamiento de los costos y de los indicadores de eficiencia de la producción pública.

El Dr. Alfredo Le Pera, en noviembre de 2003 presentó publicado una investigación titulada Trabajos Técnicos Nacionales, Ciclo Presupuestario Integrado Predeterminación de Costos en el Sector Público.

A efectos de concretar su trabajo el autor tomó en consideración los siguientes sistemas:

1) Presupuesto

2) Inversiones

3) Crédito Público

4) Tesorería

5) Contabilidad

6) Administración de Bienes

7) Contrataciones

8) Administración Tributaria

9) Control interno y externo

Desarrolló los siguientes aspectos:

a) Los sistemas de presupuesto, de contabilidad y los costos

-

Métodos de predeterminación y determinación de costos:

b.1) Normalizadores o estándares

b.2) Directos e indirectos

b.3) Absorción

b.4) Órdenes

b.5) Procesos

10) Costos fijos, semifijos y variables

11) Cierre del Ejercicio.

Todos los conceptos señalados precedentemente son avalados por un Ejercicio Práctico Integral, con sus correspondientes asientos por partida doble, incluyendo:

a) Resultados de la ejecución fiscal.

b) Determinación del Cuadro de Ahorro-Inversión-Necesidad de Financiamiento

c) Análisis de gestión

d) Reflexiones.

Siguiendo con el trabajo del Dr. Alfredo Le Pera, se considera relevante transcribir los siguientes conceptos:

Sobre los sistemas de presupuesto y de contabilidad de costos:

La eficacia y eficiencia del gasto requieren predeterminación y determinación de los costos de producción públicos.

Los costos deben:

a) Predeterminarse en el presupuesto

b) Determinarse en la contabilidad.

Ambos deben brindar los informes necesarios para el control de gestión a cargo de las autoridades superiores de las organizaciones y de los órganos específicos de control interno y externo, además de los controles de cumplimiento normativo y de tipo financiero que incluye rendición y análisis de cuentas.

Métodos de predeterminación y determinación de costos

Las técnicas de medición de costos ex-ante y ex-post que se emplean en la actividad privada son utilizables.

Los cursos de acción sólo difieren de los privados en los fines de la producción y en el modo de obtención de los factores productivos.

Son aplicables, entre otros, los siguientes métodos:

a) Normalizadores o estándares

b) Directos e indirectos

c) Absorción (incluye Activity Based Costing - ABC)

d) Órdenes

e) Procesos

a) Normalizadotes o estándares

Sin fijados ex ante basados en procesos eficientes de producción con relación a un volumen dado y luego se determinan ex post comprándolos entre sí, comprobando desvíos y analizándolos.

Relacionan, para un producto esperado, las 2 variables esenciales, insumo-producto en la formulación y en la ejecución del ejercicio.

Intervienen conocimientos y habilidades relativos cada tipo de producción para lograr la mejor combinación posible de factores productivos.

En la ejecución se comprueba la calidad del estándar y la real utilización de los insumos programados.

b) Directos e indirectos

Son directos los costos previstos y luego ocurridos en la producción final que satisface las necesidades de la comunidad: Ejemplos: Salud, Educción.

Son indirectos los necesarios para producir bienes y servicios intermedios requeridos para la producción final. Ejemplo: Administración General.

-

Absorción

Se prorratean los costos indirectos sobre los directos. Las bases de distribución son variadas. Ejemplo: Consumo de energía, personal ocupado.

Hace posible conocer el costo real de las acciones productivas.

Es un procedimiento complejo y discrecional.

Un método de absorción es el ABC - Activity Based Costing.

Permite la asignación y distribución de los costos indirectos de acuerdo a las acciones realizadas, identificando el origen del costo en los cursos de acción.

Se fundamenta en que las acciones requeridas que se desarrollan en las jurisdicciones y entidades son las que consumen los recursos y originan costos, y no los productos que sólo demandan las acciones requeridas para su producción.

ABC constituye un sistema integral de gestión.

Las bases de imputación se relacionan con la medición de las acciones a desarrollar y desarrolladas.

ABC mejora la visión de los cursos de acción ya que traza el mapa de la red de acciones productivas y sus costos e identifica los que proporcionan bajo o nulo valor agregado, con el fin de eliminarlos y concentrar el peso de la gestión en los de más alto rendimiento.

En Administración se sugiere aplicarlo parcialmente, sin prorrateo.

En este trabajo se asocian costos a los cursos de acción pero no se prorratean los indirectos.

-

Órdenes

Es aplicable a acciones destinadas a producir bienes de capital o servicios individualizables. Ejemplo: Construcciones navales del Astillero Río Santiago de la Provincia de Buenos Aires; un viaje comercial de un buque de Transporte Navales.

-

Procesos

Es el más apropiado para jurisdicciones o entidades que desarrollan ciclos continuos de producción. Ejemplo: Elaboración de oxígeno medicinal para hospitales.

Costos fijos, semifijos y variables.

Esta tipificación es importante para el logro de la eficiencia cuando se exige, como en la legislación Argentina, el cierre financiero equilibrado.

A continuación señalamos el tipo de costo con el volumen de insumos.

Costo Fijo: Es indiferente a los cambios en los volúmenes de producción fijados entre un mínimo y un máximo.

Costo semifijo: Varía al cambiar el volumen de producción, siempre que el factor que se altera es un:

a) cambio en el tiempo de trabajo

-

sobre o sub aprovechamiento de los bienes de uso por haber variado la velocidad del flujo.

Costo Variable: Aumenta o disminuye correlativamente con el aumento o disminución del producto.

Se debe lograr equilibrio, entre ellos, ante los diferentes niveles de producción. Si se asignan insuficientes item variables, disminuye o se paraliza la producción y se siguen incurriendo en los mismos gastos fijos y semifijos. Éstos resultan poco útiles, o peor aún, inútiles.

Algunas reflexiones

1. La Administración Financiera (AF) tiene por objeto lograr eficiencia en la captación de los ingresos y en su utilización en la actividad productiva.

Es aceptado que la legitimidad de los gobiernos además de fundamentarse en las normas (constitucionales y legales) y en la prestación de los servicios (actividad productiva) debe basarse también en la eficiencia.

2. Un aporte importante para el logro de la eficacia y la eficiencia es la aplicación de la teoría general de sistemas en la AF. Se opera considerando las interrelaciones y condicionamientos recíprocos de cada sistema componente de la AF.

3. La eficiencia, requiere medición y evaluación previa, coetánea y posterior de los resultados en términos de productos y de costos de producción.

4. El sistema de contabilidad debe brindar la información para el control de gestión de las autoridades superiores de las organizaciones y de los órganos específicos de control interno y externo.

5. El control de gestión se suma a los controles de legalidad y financieros. Estos deben continuarse. Los tres tipos de control se complementan.

6. El control de gestión requiere la predeterminación y determinación de costos de la producción.

7. La consideración de los gastos con gravitación financiera es insuficiente en costos; sólo se prevén:

a) gastos financieros a efectuar (constituirán obligaciones a pagar)

b) recursos financieros a realizar (brindarán los medios de pago de las obligaciones a contraer).

Por lo tanto, se deben incorporar, como mínimo, el cómputo de las depreciaciones del capital amortizable y la variación de acopios de bienes de consumo. También en este trabajo se computa el interés del capital real poseído y, simultáneamente, para no afectar el resultado variación del patrimonio neto, se lo considera en la cuenta corriente como un ingreso corriente sin gravitación financiera.

8. La incorporación de los datos citados precedentemente hace posible la previsión y la comprobación sistémica de la eficiencia.

9. Los ítem de costos deben definirse homogéneamente como cuentas de los clasificadores y de la contabilidad general.

10. Las técnicas de medición de costos ex - ante y ex post que se emplean en la actividad privada son utilizables, entre otros:

a) estimados o estándares;

b) directos e indirectos;

c) por absorción (incluye ABC);

d) por órdenes;

e) por procesos.

Lo que difiere de la privada son los tipos y las razones de la producción.

11. La clasificación de la variabilidad del requerimiento en función del nivel de actividad del organismo ayuda a definir la prioridad de los distintos insumos que se requieren, pues permite en cada centro de asignación de recursos:

a) fijar la dimensión más económica.

b) mensurar cuanto se utiliza de la capacidad productiva.

c) determinar el peso negativo de la paralización de la producción.

d) establecer el costo de iniciación de actividades.

12. Se debe lograr el equilibrio entre los distintos tipos de gastos (fijos, semifijos y variables) ante los diferentes niveles de producción.

Si se asignan insuficientes ítem variables, disminuye o se paraliza la producción y se siguen incurriendo en los mismos gastos fijos y semifijos. Éstos por lo tanto resultan poco útiles, o peor aún, inútiles.

13. La experiencia Argentina en cuanto a estabilidad demuestra que el equilibrio fiscal es un requisito primario para lograrla y mantenerla.

14. Un medio para el cierre equilibrado es la programación de la ejecución. Se fijan cuotas trimestrales o de menor lapso, anticipadas, para autorizar compromisos (básicamente autorizaciones para contratar gastos) a la luz de los ingresos efectivos esperados, obligaciones a pagar y existencias de Caja.

El cierre financiero debe ser equilibrado (gastos incurridos que generan obligación de pago inmediato o de corto plazo menores o iguales que los ingresos recaudados para atenderlos).

15. Si la recaudación cae, se reducen las cuotas, entre otras medidas posibles. Si las quitas se hacen en %, se tiende a cubrir costos fijos sin atender los variables indispensables para operar. Por lo tanto los costos fijos se tornan parcial o totalmente inútiles.

16. El remedio consiste en dar cuota a los 3 tipos de costos para programas prioritarios con el fin de lograr una producción razonable. Simultáneamente, se deben desafectar programas de menor prioridad. Esta operatoria es difícil por la rigidez de adaptación de algunos factores productivos, especialmente el trabajo. Pese a ello, como el cierre equilibrado es basamento de la estabilidad, se deben hacer los esfuerzos posibles.

17. En este trabajo se utiliza costeo directo, por no ser necesario para el análisis de gestión absorber costos indirectos; se analizan también los gastos fijos, semifijos y variables.

18. En el ejemplo puede observarse como una disminución leve de las cuotas que afecta a los gastos variables degrada en un grado más que proporcional el producto final obtenido.

19. El progreso en materia de eficacia y eficiencia del gasto exige que el sistema de contabilidad integre costos.

El Dr. José María Las Heras al tratar el tema de costos - gastos y en particular: Las Técnicas de Estimación en su libro Estado Eficiente - Editorial Buyatti, señala:

Concepto e importancia:

-

Estimar no es lo mismo que evaluar el gasto, aunque suele utilizarse indiscriminadamente uno y otro término.

-

La estimación se refiere a la previsión de un gasto a realizar en el futuro.

-

La evaluación comprende el conjunto de procedimientos destinados a analizar críticamente la performance de un gasto ya realizado.

-

En materia de administración financiera (en el ámbito público) un buen presupuesto es condición necesaria, pero no suficiente. Es indispensable además un excelente sistema contable que muestre la calidad de su ejecución.

-

Todo gasto debe analizarse por si en función de un criterio situacional, (no incremental) teniendo en cuenta múltiples aspectos en su relación con el objetivo a lograr, e la mejor técnica productiva, el reflejo de los cambios en los precios relativos de los insumos, entre los puntos más importantes a considerar.

-

Esta cuestión no se circunscribe a países con escasa cultura presupuestaria, como el caso argentino. También se dá en países desarrollados.

Técnicas de estimación del gasto:

-

Técnica del costeo

-

Punto de equilibrio

-

Técnica Base Cero (x)

Con respecto a la técnica de Presupuesto Base Cero nos ocupamos en detalle, incluyendo ejemplificación práctica en el mencionado Libro Casos Prácticos de Contabilidad Pública que oportunamente publicara Editorial Macchi, no obstante se incorporan al presente material de otros destacados profesionales en la materia.

1) Técnica del costeo: Deben tomarse en cuenta:

-

Materias primas

-

Mano de obra

-

Costos de fabricación

Con estos componentes tenemos las interrelaciones sistémicas:

-

Costo primo

-

Costo de conversión

-

Costo de producción

-

Costo de comercialización

-

Costo de estructura

1) Materias primas + Mano de obra = COSTO PRIMO

2) Costo primo + Gastos indirectos de fabricación = COSTO DE PRODUCCIÓN

3) Mano de obra + Gastos indirectos de fabricación = COSTO DE CONVERSIÓN

4) Gastos de comercialización + Gastos de administración + Gastos de estructura = GASTOS TOTALES

Explicitado en otros términos podemos señalar:

GASTOS TOTALES + COSTO DE PRODUCCION = COSTO TOTAL

El costo según el nivel de actividad: debemos tener en cuenta:

1) Costos fijos - 2) Costos variables

Costos fijos: son independientes del nivel de producción pública. Se mantienen constantes, como sería el caso del alquiler del aula, concurran una o varias personas.

Costos variables: son dependientes del nivel de producción, crecen en forma proporcional o menos proporcional al nivel de producción pública. Por ejemplo el material que se entrega en relación de los asistentes.

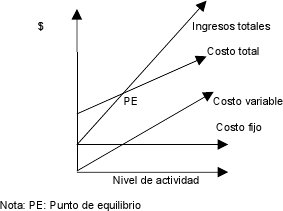

2. Punto de equilibrio: Se consideran

Los montos - Nivel de actividad - Costos Fijos Costos Variables - Costo total

Mediante su representación gráfica se permite visualizar las áreas de ganancias y las áreas de pérdidas de un programa, de un proyecto, etc.

Se entiende como punto de equilibrio la intersección entre el total de costos o de gastos (según el caso) y el total de ingresos.

3) Técnica Base Cero

Fases del proceso

Fase I : Líneas políticas y pautas de acción

Fase II: Identificación de las unidades de organización

Fase III: Paquetes de decisión

Integración de los paquetes

a) Objetivos

b) Metas

c) Costos

d) Beneficios

Niveles de actividad

1) Normal

2) Mínimo

3) Superior

4) Optimo

Fase IV: Ordenamiento de los paquetes de decisión

Según el Dr. Humberto Petrei: el Presupuesto Base Cero es complementario del Presupuesto Por Programas.

La Dra. Lea Cristina Cortes de Trejo en su trabajo Costos para la gestion en el sector publico, presentado en el Seminario Regional Interamericano de Contabilidad - Córdoba 2001, señala como Objetivos de la Contabilidad de Costos los siguientes aspectos

Llevados al sector público, los objetivos de la Contabilidad de Costos, consisten en:

-

Optimizar el empleo de los recursos públicos desde la perspectiva de la eficacia, eficiencia y economía, posibilitando el control de gestión y minimizando las cargas tributarias del contribuyente.

-

Suministrar información para la planificación, el control y la toma de decisiones en el Sector Público, siendo la base para la formulación y evaluación de los presupuestos públicos, contribuyendo al equilibrio fiscal y a una mayor producción en el accionar estatal.

-

Determinar el costo de las actividades y de la prestación de servicios públicos (fijación de precios y tarifas).

-

Hacer eficaz, eficiente y económico el sistema de información del ente, en general, y el de contabilidad, en particular.

-

Brindar información útil a usuarios internos y externos, apoyando la toma de decisiones sobre la producción de bienes y servicios públicos en términos de calidad.

-

Coadyuvar a la transparencia fiscal, dado que al ciudadano le interesa cada vez más evitar desperdicios, ineficiencias y malversaciones en el uso de los recursos públicos.

-

Promover la responsabilidad de los funcionarios en términos de productividad de sus servicios a un costo y calidad óptimas.

Asimismo en la misma presentación señala como Condicionantes de la Contabilidad de Costos en el Sector Público lo siguiente:

La instrumentación de la contabilidad de costos en el Sector Público depende de factores particulares que condicionan ese proceso, entre los cuales se encuentran:

-

Marco político - normativo.

-

Modernización de la Administración Pública.

-

Características distintivas entre las haciendas públicas y las haciendas privadas.

-

Entorno de la Contabilidad Gubernamental.

-

Necesidades e intereses de los usuarios.

-

Los componentes del Sector Público.

-

Los sistemas de control interno y externo.

-

Acceso a la financiación y a equipamientos informáticos adecuados.

Antes volcar las conclusiones de este trabajo, nada mejor que recordar las palabras que el Dr. José Terry en su carácter de catedrático nos legara en una conferencia de 1897, que tienen plena vigencia, por lo tanto considero oportuno transcribir algunos de sus párrafos:

Donde hay un gasto debe haber una necesidad.

En el presupuesto se aprueban en el primer artículo esos gastos y el en segundo se encuentran las principales fuentes que producen la renta del Estado.

Puede decirse que después de la Ley fundamental de nuestro país que es la Constitución Nacional, la más importante es la del presupuesto porque sirve de autorización y compromiso entre el Contribuyente, el pueblo (mandante) que por sus representantes determina al Gobierno Mandatario lo que ha de gastar y lo que no debe gastar, y en que necesidades debe aplicar los recursos que se votan.

El Gobierno maneja dinero ajenos, y en consecuencia, debe subordinarse en todo a las instrucciones del dueño de ese dinero, es un serio compromiso, faltar a él, es cargar graves responsabilidades.

Puede compararse el presupuesto al espejo donde se reproduce fielmente la vida de toda una Nación.

El Presupuesto es necesario porque sirve al programa para la marcha del país, con el presupuesto se establecen las mejoras y los adelantos por hacer en el año venidero, las necesidades que han de llenarse y los progresos que han de realizarse.

¿Quién debe votar los recursos?. El que los suministra; es decir el contribuyente, el pueblo por medio de sus representantes.

Este es el principio fundamental en todo sistema de gobierno libre, y es de aplicación casi universal.

El gran principio del voto del recurso, trae como consecuencia, el voto de la necesidad y del gasto correspondiente.

El poder de conceder el recurso importa el poder de autorizar el gasto.

Quién vota la contribución tiene que votar el gasto.

Importa algo más: la de poder apreciar si el recurso otorgado ha sido publicitado y en el gasto autorizado, que debe ser publicitado.

Las precisas expresiones del Dr. Ferry eximen de toda aclaración sobre la relación entre presupuesto - gastos - costos.

También Para advertir la importancia del tema que nos ocupa, varios siglos atrás Montesquieu nos decía; Cuando en un Estado, al hablarse de la Cosa Pública, cada uno dice: ¡Que me Importa! la Cosa Pública esta perdida.

CONCLUSIONES

1. La relevancia que adquiere considerar para la toma de decisiones los Costos Fijos y los Costos Variables.

2. Tener en consideración las diferencias del tratamiento del costo que debe existir en el Sector Público con el costo en el Sector Privado. (Según Dr. Cayetano Licciardo la diferencia está en los negocios de naturaleza distinta).

3. En el Sector Público el costo no debe ser el único elemento, o sustancial elemento, a tomar en consideración por los Gobiernos para la decisión de hacer algo a favor de la población.

4. Si la competencia es del Estado (Nacional, Provincial, Municipal) el costo no debe ser quién decida si se hace o no. El beneficio debe estar sustentado en el bien común.

5. Deben aplicarse las técnicas más adecuadas que permitan posibilitar su cumplimiento.

6. Entre todas las señaladas en este trabajo podemos concluir como aporte que en su totalidad apuntan a verificar el cumplimiento de la: Eficiencia - Eficacia - Economicidad

7. Nuestra responsabilidad profesional está asentada en el logro de los objetivos, tratando de analizar cual es la técnica más adecuada a tal fin

8. En la técnica de Presupuesto por Programas que se utiliza en la actualidad sintetizamos en este cuadro las relaciones que existen entre Costos - Productos - Objetivo.

9. Por todo lo expuesto en el trabajo, la importancia del tratamiento del costo su estrecha vinculación con el gasto público que revela el cumplimiento de las Finalidades es lo que da sustento a una correcta presupuestación y su correspondiente ejecución que como se verifica en el cuadro del punto 8) concluye en el impacto que recibe la comunidad.

BIBLIOGRAFIA

1. CORTES DE TREJO L. C. (2001) "Costos para la gestión en el Sector Público" Objetivos de la Contabilidad de Costos" Seminario Regional Interamericano de Contabilidad Córdoba. [ Links ]

2. LAS HERAS M. JOSE ( 2007) Estado Eficiente Editorial Buyatti. [ Links ]

3. LE PERA A. (2005) "Ciclo Presupuestario Integrado Predeterminación de Costos en el Sector Público".Jornadas de Reflexión en Cátedras Facultad de Ciencias Económicas UBA (Cátedra de Sistemas de Administración Financiera y Control del Sector Público). "Estudio de la Administración Financiera Pública" Ediciones Cooperativas. [ Links ]

4. TIBERIO J.C.; MASTRANTONIO H. F. (1990) "Casos Prácticos de Contabilidad Pública". Editorial Macchi. [ Links ]